Write off bad debts

Find this screen

Open: Customers > Credit Control > Write Off Customer Bad Debt.

How to

Write off bad debts that you've made provision for

If you've previously made provision for an transaction, a W is displayed in the Qry column. This is done using the Provide for and Correct Customer Bad Debt screen. You provide for bad debts when you want to move the value of transactions that you want to write off in future your Balance Sheet to your Profit and Loss.

To filter the list to only show these transactions, select Display provisions only.

- Choose the customer(s) to write off transactions for:

- Select Single customer and choose the customer account from the drop-down lists.

- Select Multiple customers and enter a range using the From and To boxes.

- Choose whether you want to write off All transactions or selected transactions By date range.

- Enter the Date from and To or use the date picker

.

.

- Enter the Date from and To or use the date picker

- Select Display provisions only.

- Select each invoice that you want to write off by selecting the check box at the left hand side of the window.

- If an invoice has been part paid, enter the amount of VAT you want to reclaim.

- Click Write Off.

Write off other bad debts

- Choose the customer(s) to write off transactions for:

- Select Single customer and choose the customer account the drop-down lists

- Select Multiple customers and enter a range using the From and To boxes

- Choose whether you want to write off All transactions or selected transactions By date range.

- Enter the Date from and To or use the date picker .

- Enter the Date from and To or use the date picker

- Select each invoice that you want to write off by selecting the check box at the left hand side of the window.

- If an invoice has been part paid, enter the amount of VAT you want to reclaim.

- Click Write Off.

Write off part paid invoices

If an invoice has been part paid, you must decide the portion of the VAT that you want to reclaim. For example, if 50% of the invoice value has been paid, then you would usually reclaim 50% of the VAT.

- When you select the invoice to write off, enter the amount of VAT you're reclaiming in the VAT column.

Note: The VAT amount defaults to 0.00. If you don't change it, VAT isn't reclaimed when the invoice is written off.

Useful info

About writing off transactions

Use this when it becomes clear that a customer is not able to pay outstanding invoices and you want to write off the invoice and claim back from HMRC any VAT you have paid.

Sage 200 makes two types of transaction available for you to write off:

-

Transactions that have already been provisioned. They are indicated by a W in the Qry column.

-

Other outstanding transactions that have exceeded the bad debt waiting period.

When you choose to write off an invoice, a credit note for the same value is created and allocated to the selected invoice.

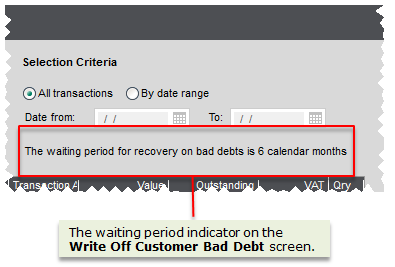

About the bad debt waiting period

You can only reclaim the VAT once the debt is more than minimum waiting period set by HMRC. This was 6 months as at January 2015. You enter this period on the Customer Settings and Defaults screen and it is displayed here.

Sage 200 lists only the transactions which are older than this period. No invoices raised within the specified period will be displayed - no matter which selection criteria you use.

About making provision for bad debts

You make provision for bad debt when you have decided to write off part, or all, of your customer's debt, but the debt is not yet old enough to fully write off and reclaim the VAT.

Under HMRC rules you can reclaim VAT you have paid on a transaction once a debt is more than six months old. However, before the transaction is six months you can indicate that you intend to write this off. This posts a transaction that moves the value of the transaction from your Profit and Loss to your Balance Sheet. This is called making provision for bad debts.

You do this to account for the value of the outstanding invoices on your Profit and Loss, rather than your Balance Sheet.

When you do this:

- You can't then allocate a receipt to that invoice.

- The invoice is marked with W query.

- The value of the invoice is posted to the Bad Debt Provision (BS) and Bad Debt Expense (PL) nominal accounts.

Once the invoice is older than the minimum waiting period, you write it off here.

When the bad debt involves foreign currency transactions

The write off is posted in your base currency using the original exchange rate set on the invoice.

If the transaction has been revalued, prior to being written off, then any exchange differences are also reversed.

You enter an invoice for $100 and the rate is $2.00 to the £. You then revalue all dollar transactions using an exchange rate of 1.5. The value of the $100 invoice has changed from £50 to £66.67, so an exchange difference of £16.67 is posted.

You subsequently choose to write off this invoice, so you also need to write off the revalued amount. Sage 200 therefore posts the following transactions:

| Nominal Account | Debit | Credit |

|---|---|---|

|

Bad Debt Provision (Balance sheet) |

50.00 | |

|

Debtors control (Profit and Loss) |

50.00 | |

| Exchange Differences | 16.67 | |

| Debtors Control | 16.67 |

Fix it

The invoice isn't shown in the list

If the invoice is less then six months old, it won't be shown here. This is because you can only write off debts and reclaim the VAT for invoices that are more than six months old.

If you don't want to reclaim the VAT, you can:

-

Write off outstanding amounts on individual invoices using the Write Off Small Amounts screen.

Open: Write Off Customer Small Amounts

-

Write off customer account balances, using the Write Off Customer screen.

Open: Write Off Customer

What happens when

A transaction is written off?

If you haven't made provision for an invoice:

-

A credit note is created and posted to the following nominal accounts:

Nominal Account Debit Credit Debtors Control

(Balance sheet)

Gross amount VAT output

(Balance sheet)

VAT amount Bad Debt Expense

(Profit and Loss)

Net amount Note:If you have specified a cost centre and department for the default sales nominal account on your

For example, if a

- The credit note is allocated to the invoice.

- If VAT was included, then the credit note is included on your next VAT Return.

A transaction that's been provided for is written off?

If you have previously made provision for the invoice:

-

A credit note is created and posted to the following nominal accounts:

Nominal Account Debit Credit Debtors Control

(Balance sheet)

Gross amount Bad Debt Provision

(Balance Sheet)

Gross amount VAT output

(Balance sheet)

VAT amount Bad Debt Expense

(Profit and Loss)

VAT amount Note:If you have specified a cost centre and department for the default sales nominal account on your

For example, if a

- The credit note is allocated to the invoice.

- If VAT was included, then the credit note is included on your next VAT Return.

Sage is providing this article for organisations to use for general guidance. Sage works hard to ensure the information is correct at the time of publication and strives to keep all supplied information up-to-date and accurate, but makes no representations or warranties of any kind—express or implied—about the ongoing accuracy, reliability, suitability, or completeness of the information provided.

The information contained within this article is not intended to be a substitute for professional advice. Sage assumes no responsibility for any action taken on the basis of the article. Any reliance you place on the information contained within the article is at your own risk. In using the article, you agree that Sage is not liable for any loss or damage whatsoever, including without limitation, any direct, indirect, consequential or incidental loss or damage, arising out of, or in connection with, the use of this information.